Datafiles Jun 17

Overall economic growth prospects for the Africa region are favourable. Most banks will raise capital base and maintain stable profitability, but weak asset quality will remain a key concern

Overall economic growth prospects for the Africa region are favourable. Most banks will raise capital base and maintain stable profitability, but weak asset quality will remain a key concern

In the Asia Pacific region, skilled and experienced tech professionalsand regulatory compliance specialists will find themselves well-positioned in the banking and financial services market

As the race towards digitalisation intensifies, the relationship between banks and “big tech” companies is increasingly marked by collaboration and synergy, not just competition

Increased utilisation of financial technology is setting the stage for further digitisation of the Philippine’s consumer banking industry, which is slowly transitioning into a “cash-lite” economy.

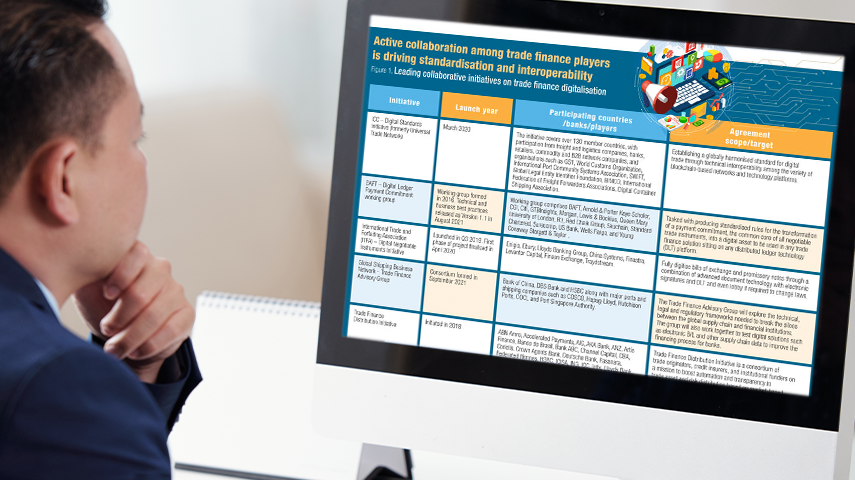

As the trade finance industry collectively progresses to address challenges around digital fragmentation and isolation, adoption of standard solutions and well-established legal frameworks along with technology as an enabler will play critical roles in truly digitalising trade.

Commercial banks such as DBS Bank and traditional exchanges such as the Singapore Exchange have one thing in common: they are setting up and adding digital exchanges and platforms to their existing business lines.

At the International Heads of Retail Finance Virtual Meeting on 28 August 2020, leaders from over 22 institutions in Asia Pacific, the Middle East and Africa, discussed key trends and issues impacting the industry. The rise of digital only banks, integrating lifestyle and finance through digital platforms, and improving customer experience were at the forefront of the dialogue.

The inaugural BankQuality™ Consumer Survey and Rankings interviewed 11,000 bank customers in 11 markets across the Asia Pacific region on their engagement, experience and satisfaction with their main retail banks.

The German fintech’s dramatic collapse is likely to reshape the payment processing landscape as market rewards players leading innovation and value creation

Indonesia is seeing exponential growth in mobile payments spurred by a robust fintech landscape, though usage remains uneven and limited

While fintechs may take some market share away in specific niches, the partnerships, analytics, and value-add that leading banks are developing can keep head of the game. Banks that fail to keep up could lose a significant share of their SME business

Several key themes emerged amidst the many discussions by global leaders in payments, including QR code, blockchain, credit card schemes, fintech and data consolidation

The banking industry in Asia Pacific will continue to be stable, but will face persistent dark clouds and headwinds. Slower growth, trade disruptions, financial asset repricing and high private sector leverage emerge as top industry risks for 2019

Driven by competition and rapid disruption, banks increasingly spend on technology enabled models targeted to improve customer experience and service capability. What are the recent developments and top priorities of banks in 2018?

Global and regional cash management banks across Asia-Pacific are making substantial investments in digital initiatives to enhance the overall transaction experience of their clients.

The discussion on cybersecurity is being given increased importance in the boardroom as cybercrime goes global and data protection comes to the forefront

Implications of new regulations and emergence of digital-only players were hot button issues discussed this year at the Asian Banker Future of Finance ‘Global Transactions Re-invented’ track

Pundits who see fintechs as the epitome of digital revolution need to pause and consider a simple fact, they may well be transitory and more dramatic changes are yet to come

Long a bastion of personalised service by relationship managers, the wealth management sector is undergoing a transformation as clients demand better service and as digital delivery enables new models. Wealth management firms need to combine “high-tech” with “high-touch” to stay ahead.

Traditional banks in China have begun to utilise cutting-edge technologies by collaborating with technology companies, start-ups or emerging financial institutions. While pushing their way in revolution, the vital point is to strike a balance between the digitisation of services and traditional manual banking services.

The last four years have been considered the worst for Thai banks in retail banking. Despite a meagre income and loan growth, banks have been working hard to improve operating efficiencies, re-balance portfolios, and build digital platforms to support the country’s next phase in e-payments, internet financing and micro lending.

Economies of scale, profitability, and developing a comprehensive service proposition remain major challenges in Vietnam’s growing retail banking industry. A long-term sustainable future will depend on how banks execute a right risk-reward balance

Retail banks in Hong Kong are capitalising on fintech to innovate their product palate and to reach out to new customers through dedicated digital channels.

Mobile payment apps have continued to proliferate in countries around the world, with Mercedes Pay soon likely to join the more familiar Apple Pay and Samsung Pay. Local apps in Asia, ranging from Paylah! in Singapore to Kakao in South Korea, offer mobile payments as well.

The evolving landscape of South Korean retail banking is pushing banks to invest in financial technology to retain and attract customers, even as traditional brick and mortar branches give way to specialised branches.

In the quest to create financial ecosystems, banks believe they can stay relevant to a customer’s financial needs.

Taiwan’s Financial Supervisory Commission (FSC) is driving the country’s banks to move to digital platforms through its “Bank 3.0” vision as banks have an urgent need to differentiate themselves in the crowded retail banking market.

With more than 70% of Southeast Asia being unbanked, fintech possesses tremendous potential to widen financial inclusion and spur economies. Advances in the industry mean more people and companies have the ability to save, borrow and transact. Yet with such a wide and sensitive remit, regulations need to keep pace with the constant innovation.

Financial institutions are starting to use APIs to create important linkages between their products and services and their customers and important third party value providers. Early movers to stand to gain mindshare of both customers and the wider application developer community.

Fintech, the latest buzzword in the peer-to-peer lending sector, has carved a niche for itself in a short span of time. As banks tighten their seat belts for the new-age disruption, they are showing strong affinity towards collaboration with the marketplace lenders to secure their customer proposition.

Customised financial advice had, for many years, been available almost exclusively to private banking clients or to the mass affluent. However, robo-advisors are offering the same advice to many more consumers. Customers in Asia, from the man on the street to the ultra-wealthy, seem ready to embrace these new robo-advisors.

Digitisation in the cross-border money transfer industry might leave fewer opportunities for incumbent banks and operators to grow. How they cultivate alliances and digital innovation to stay ahead of competitive will be critical moving forward.

New proofs of concepts have emerged in blockchain as the industry tackles various impediments to its successful adoption. The technology initiatives would need to be complemented with stronger collaborative efforts and interoperability for future growth.

.png)

Wide discontent with conventional banks have led to the emergence of mobile-only fintech banks. However, these challenger banks are struggling to expand their customer reach, putting doubts whether they can stand against bigger traditional banks.

It is not often that a technology comes along that forces a rethink of traditional business models. Blockchain, a technology that originated from an anti-establishment alternative to fiat currencies, is fast finding applications in a myriad of financial use cases

The incumbent outlines its response to an increasingly fragmenting payments landscape offering to support old and new customers alike by helping them de-risk major technology investments with the provision of a gateway service.

Regulators in Asia Pacific such as Indonesia's OJK are actively planning for measures to promote the growth of fintech in the region.

The development of digital platforms that enable direct global money transfer is a nascent but fast growing business model from the remittance industry. The model does not envisage traditional banks as part of the long term plans, and competes with the largest global money operators head on.

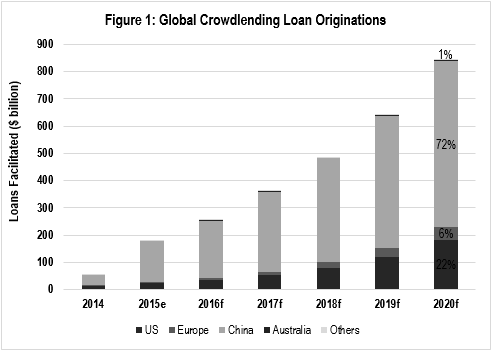

While crowdlending in Asia Pacific shows early promise, its fate will be dictated by how regulators and banks respond to the challenges they pose.

Banks are integrating new technologies into their core businesses to improve their digital banking presence and speed-to-deliver

The rapid digitalisation of MSMEs, emergence of new digital-native business models and niche segments have become a key focus area for financial technology companies to serve.

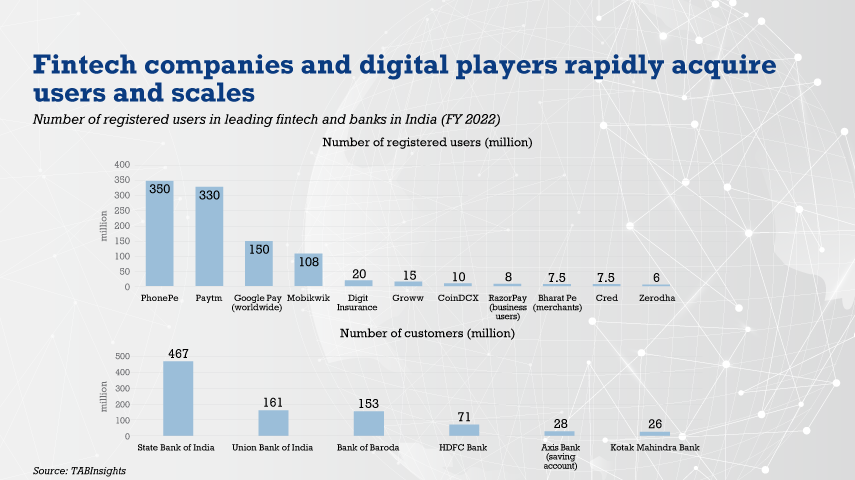

Growing transaction volumes are pushing Indian banks to rethink technology architecture to integrate cloud and data capabilities to meet growing transaction volumes. Indian fintechs and digital players see consumer growth, but also increased expectations and competition.

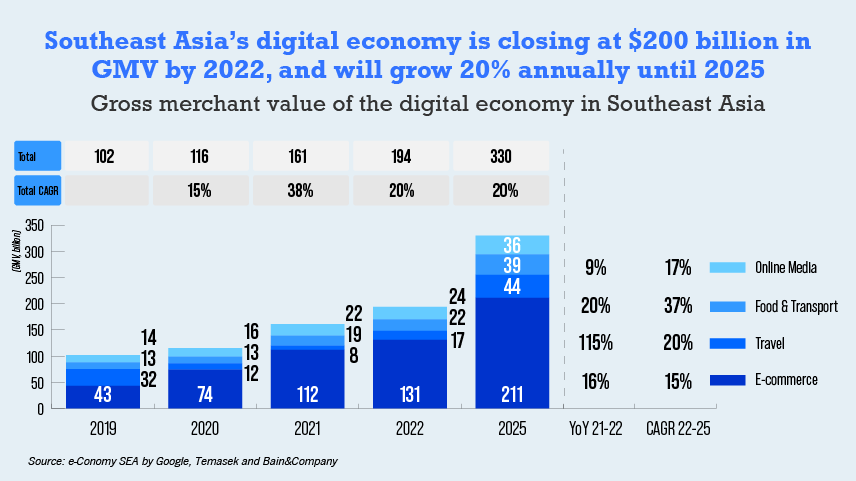

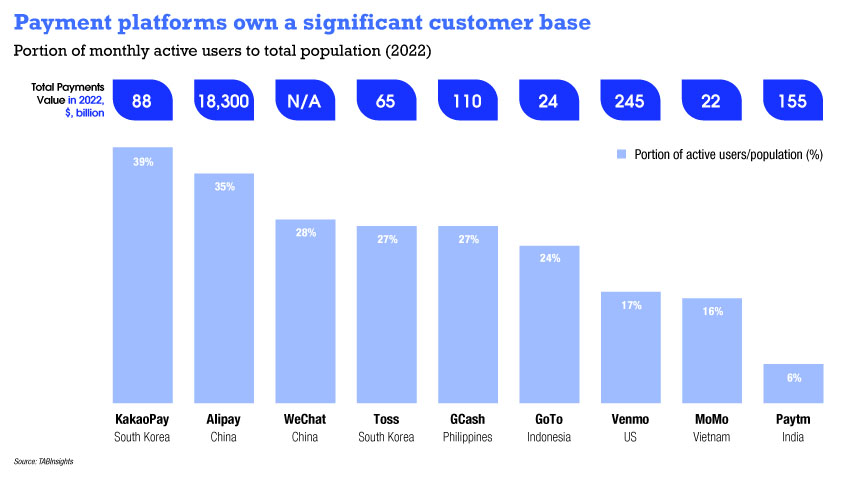

The current disintermediation in payments and MSME lending marks the tip of the iceberg, and retail deposits may be the next battleground

With a large portion of Africa’s population still lacking access to traditional banking services, particularly in places banks fear to tread, payment providers have stepped into the breach, gaining in popularity for offering services beyond the usual payments, money transfer and savings

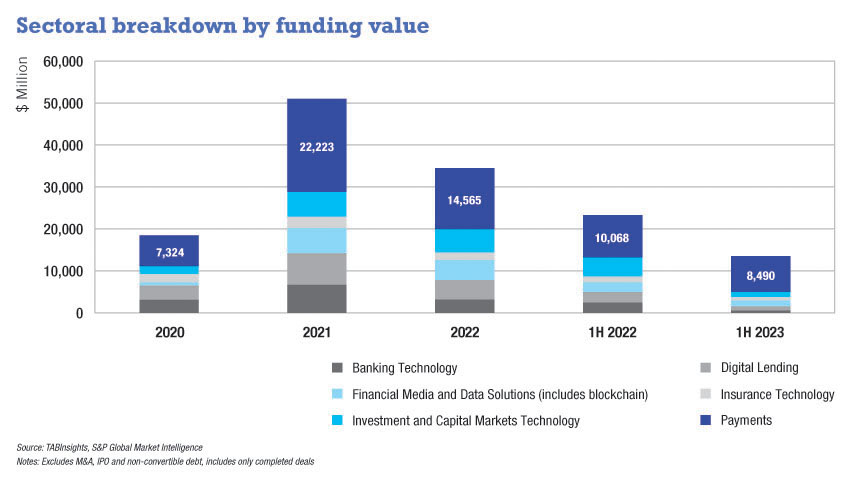

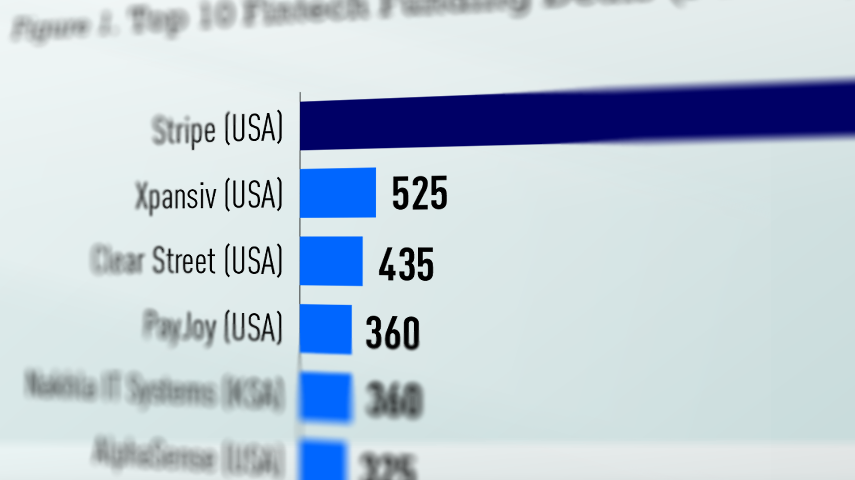

Investors’ risk appetite and fondness for fintechs have cooled, leading to a 42% drop in global funding and 57% drop in APAC funding in the first half of this year

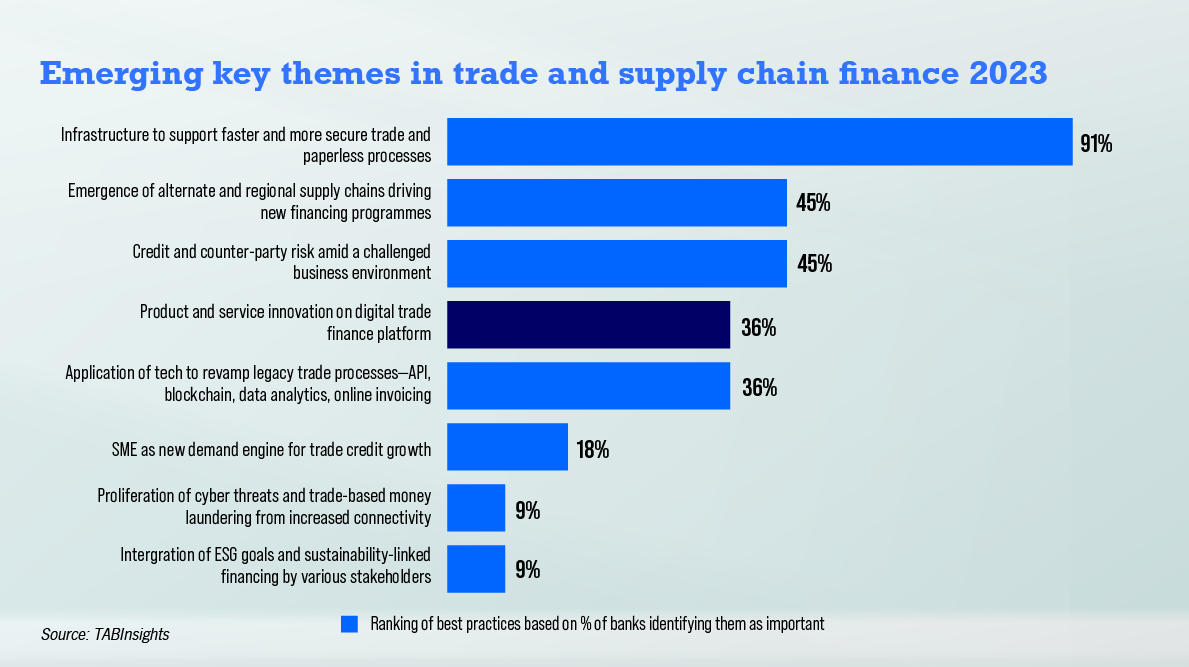

The shift in global supply chains is accelerating demand for new financing programmes and solutions that aim to accelerate and improve trade digitalisation processes

Trade finance is gradually digitalising amid evolving e-commerce models, driven by technology and sustainability; the $2.5 trillion global trade finance gap affecting SMEs prompts innovation in blockchain, tokenisation, and sustainability, despite geopolitical complexities

Transaction banks in the Middle East are expanding services in non-oil businesses with high growth potential, in line with economic diversification, and to mitigate geopolitical instability in countries in the Gulf Cooperation Council

Fintech funding dropped 42% in 2023 due to economic challenges, yet top firms like Stripe and Investree saw significant investments, demonstrating resilience amid market volatility and uncertainty

© Copyright , TABInsights. All Rights Reserved